- Scotiabank

- National Bank

- RBC

- CIBC

- BMO

- TD

From RBC to TD, Canada’s major banks posted fourth-quarter earnings this week, highlighting shifting profits, credit trends, and signals for investors. The post Stock news for investors: Fourth-quarter earnings roll in from Canada’s big banks appeared first on MoneySense.From RBC to TD, Canada’s major banks posted fourth-quarter earnings this week, highlighting shifting profits, credit trends, and signals for investors. The post Stock news for investors: Fourth-quarter earnings roll in from Canada’s big banks appeared first on MoneySense.

Stock news for investors: Fourth-quarter earnings roll in from Canada’s big banks

Featured RRSP Accounts

featured

EQ Bank

Build your retirement savings with 1.50% interest, tax-deferred contributions and zero fees.

go to site

featured

Registered GIC rate

Earn a guaranteed 2.75% in your RRSP when you lock in for 1 year.

go to site

Best RRSP rates

See our ranking of the best RRSP accounts and rates available in Canada.

read now

MoneySense is an award-winning magazine, helping Canadians navigate money matters since 1999. Our editorial team of trained journalists works closely with leading personal finance experts in Canada. To help you find the best financial products, we compare the offerings from over 12 major institutions, including banks, credit unions and card issuers. Learn more about our advertising and trusted partners.

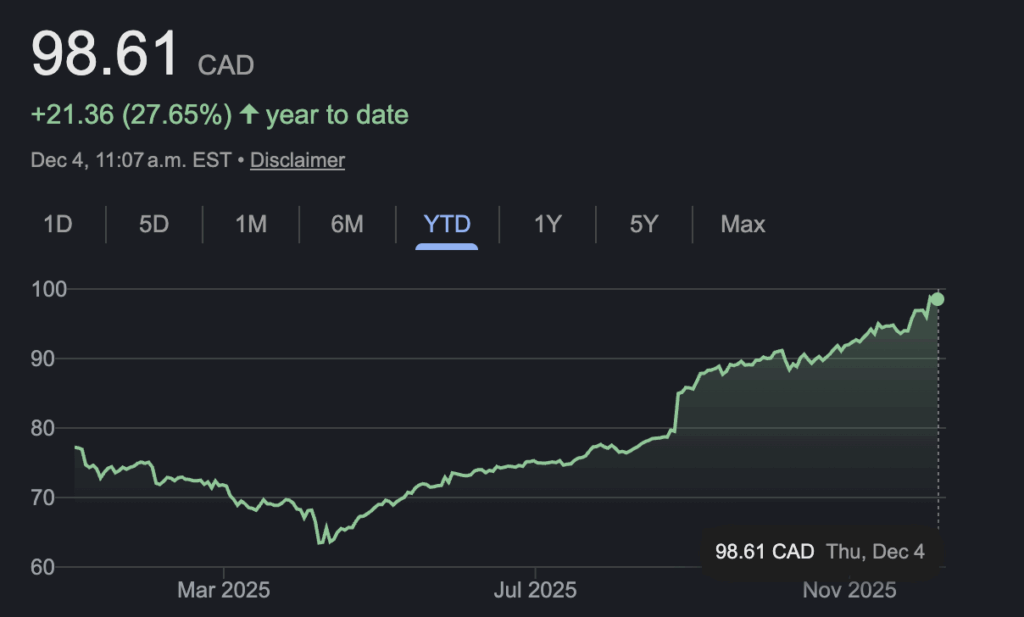

Scotiabank reports $2.21B Q4 profit up from $1.69B a year ago

Scotiabank (TSX:BNS)

Numbers for its fourth quarter:

- Profit: $2.21 billion (up from $1.69 billion a year ago)

- Revenue: $9.80 billion (up from $8.53 billion)

Scotiabank says it earned $2.21 billion in net income for its fourth quarter, up from $1.69 billion in the same quarter last year, helped by strength in its wealth management and capital markets businesses. The bank said Tuesday the profit amounted to $1.65 per diluted share for the quarter ended Oct. 31, up from $1.22 per diluted share in the same period a year ago.

Revenue totalled $9.80 billion, up from $8.53 billion in the same quarter last year. The bank’s provision for credit losses amounted to $1.11 billion for the quarter, up from $1.03 billion a year ago.

On an adjusted basis, Scotiabank says it earned $1.93 per diluted share in its latest quarter, up from an adjusted profit of $1.57 per diluted share a year ago. Analysts on average had expected an adjusted profit of $1.84, according to estimates compiled by LSEG Data & Analytics.

Scotiabank chief executive Scott Thomson said 2025 was a very positive year for the bank. “We delivered improving results through the year as we strengthened our balance sheet, improved our loan-to-deposit ratio, and increased return on equity,” Thomson said in a statement. “This quarter all our business lines reported year-over-year earnings growth with particular strength in global wealth management and global banking and markets and improving results in Canadian banking.”

The bank’s global wealth management business earned $447 million in net income attributable to equity holders, up from $380 million in the same quarter last year, while its global banking and markets business earned $519 million for the quarter, up from $347 million a year ago.

Scotiabank’s Canadian banking operations earned $941 million in its latest quarter, up from $934 million in the same quarter last year. Meanwhile, Scotiabank’s international banking arm earned $634 million in net income attributable to equity holders of the bank for the quarter, up from $600 million a year ago.

Source Google

Source Google

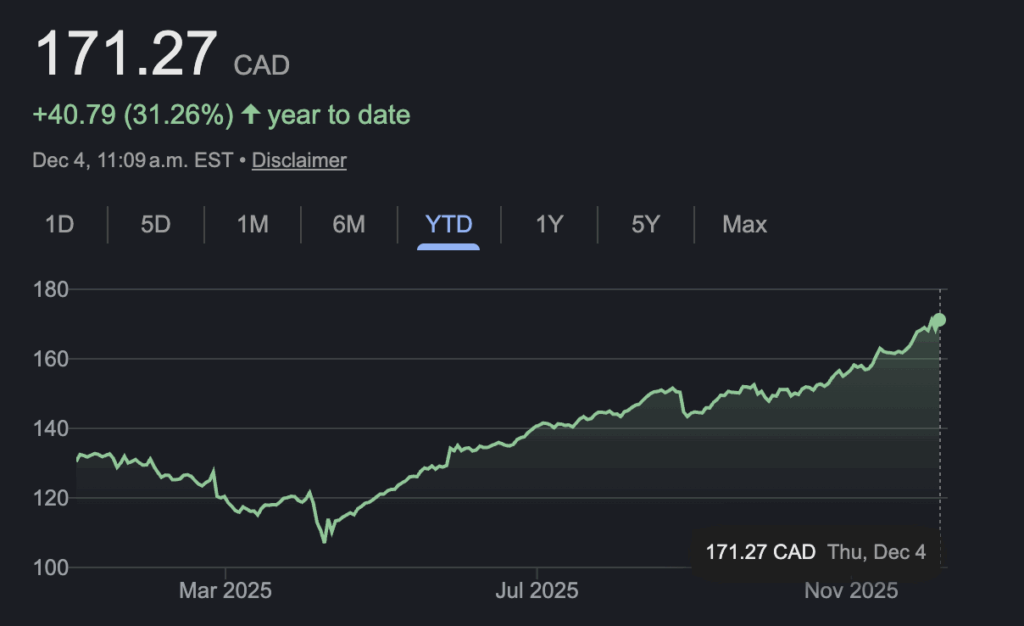

National Bank reports $1.06B fourth-quarter profit, raises dividend

National Bank of Canada (TSX:NA)

Numbers for its fourth quarter:

- Profit: $1.06 billion (up from $955 million a year ago)

- Revenue: $3.70 billion (up from $2.94 billion)

National Bank of Canada raised its dividend as it reported a fourth-quarter profit of $1.06 billion. The bank said Wednesday it will now pay a quarterly dividend of $1.24 per share, an increase of six cents.

National Bank, which announced Tuesday that it was buying Laurentian Bank’s retail and small business segments, says its fourth-quarter profit amounted to $2.57 per diluted share, compared with net income of $955 million or $2.66 per diluted share a year ago when it had fewer shares outstanding.

Revenue for the quarter ended Oct. 31 totalled $3.70 billion, up from $2.94 billion a year earlier.

The bank’s provisions for credit losses amounted to $244 million, up from $162 million in the same quarter last year. On an adjusted basis, National Bank says it earned $2.82 per diluted share in its latest quarter, up from an adjusted profit of $2.58 per diluted share in the same quarter last year. Analysts on average had expected an adjusted profit of $2.62 per share, according to estimates compiled by LSEG Data & Analytics.

“With our strengthened national presence, diversified business mix, strong capital ratios and prudent credit profile, we are well-positioned to generate continued growth and superior returns, in what will remain a complex macro-environment,” National Bank chief executive Laurent Ferreira said in a statement.

The bank said its personal and commercial banking group earned $319 million in its latest quarter, down from $327 million a year ago, as it was hit by costs related to the acquisition of Canadian Western Bank.

National Bank’s wealth management business earned $258 million, up from $219 million, while its capital markets arm earned $432 million, up from $306 million.

National Bank’s U.S. specialty finance and international operations earned $174 million, up from $157 million in the same quarter last year.

Source Google

Source Google

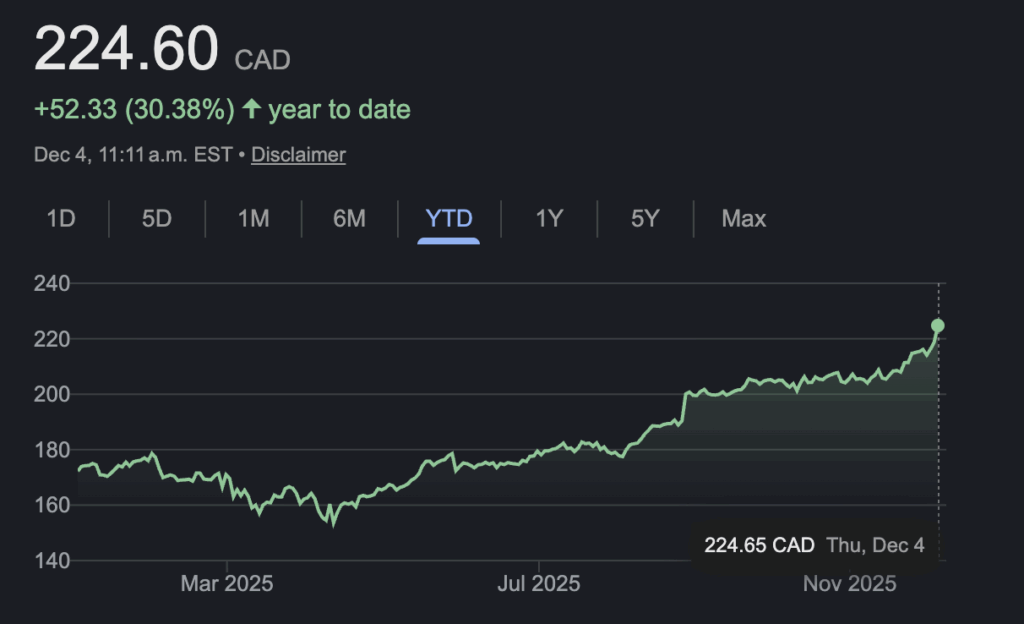

RBC posts record Q4 profit but CEO raises concerns about uneven economic recovery

Royal Bank of Canada (TSX:RY)

Numbers for its fourth quarter:

- Profit: $5.43 billion (up from $4.22 billion a year ago)

- Revenue: $17.21 billion (up from $15.07 billion)

Royal Bank of Canada handily beat analyst expectations as it reported record fourth-quarter results that showed rising profits across most divisions.

The bank said Wednesday it made a profit of $5.43 billion in the quarter ending Oct. 31, up from a profit of $4.22 billion a year ago, as capital markets, wealth management and personal and commercial banking all saw higher returns, offset by lower results in insurance. The results helped lead RBC to increase its quarterly dividend to $1.64 per share, up from $1.54 per share.

The bank sees continued strength ahead, raising its return-on-equity target to 17 per cent, up from 16 per cent.

RBC’s results and outlook come despite continued trade and economic uncertainty, but chief executive Dave McKay expressed cautious optimism on the wider picture. “While the operating environment remains fluid and complex, and there is a lot of hard work yet to be done by governments and the private sector, I am cautiously optimistic on the outlook for Canada,” he said on an earnings call with analysts Wednesday.

McKay noted that overall Canada’s effective tariff rate remains low and has done little to impact exports to the U.S., while the ongoing shift to a service-oriented economy should also offset some trade-related headwinds. He did, however, express concern with the split economic recovery, which is leading to increased inequality.

“The impact of the K-shaped economy is increasingly polarizing, with more affluent consumers investing disposable income and growing markets, while less affluent consumers struggle with affordability.” The trend can be seen in RBC’s own results, with its capital markets and wealth management divisions driving much of the earnings beat.

Meanwhile, many borrowers continue to struggle, with the bank increasing its provisions for potentially bad loans in the quarter to $1.01 billion, up from $840 million a year ago.

Chief risk officer Graeme Hepworth said the overall Canadian economy has demonstrated strong resilience this past year with household spending strong, but the bank has maintained a prudent approach to provisions given trade issues are largely unresolved and pockets of concern remain.

“Rising unemployment in Ontario and the Greater Toronto Area, coupled with higher payments at mortgage renewal, have contributed to rising consumer impairments in these regions,” said Hepworth. “We expect retail losses to remain elevated in 2026 as we work through the lag effect of higher unemployment, consumer insolvencies, and ongoing payment shocks for mortgage renewals in Canada.”

The areas of concern did little to hold back overall results, with adjusted earnings of $3.85 per diluted share in the quarter, up from an adjusted profit of $3.07 per diluted share in the same quarter last year.

Analysts on average had expected an adjusted profit of $3.53 per share, according to estimates compiled by LSEG Data & Analytics.

Scotiabank analyst Mike Rizvanovic said that while credit losses were elevated, they remained manageable as other areas like capital markets and wealth shined. “A strong quarter overall for (Royal Bank) at first look, driven by outsized growth in the top line that benefited once again from solid gains in market-sensitive businesses, which comfortably offset a modest miss across other business lines,” he said in a note.

Revenue totalled $17.21 billion, up from $15.07 billion in the same quarter last year.

RBC’s wealth management arm earned $1.28 billion, up from $969 million a year ago, while the bank’s capital markets business earned $1.43 billion, up from $985 million in the same quarter last year. Personal banking earned $1.89 billion in the bank’s latest quarter, up from $1.58 billion a year ago. Commercial banking operations earned $810 million, up from $774 million. RBC’s insurance business earned $98 million, down from $162 million a year ago.

Source Google

Source Google

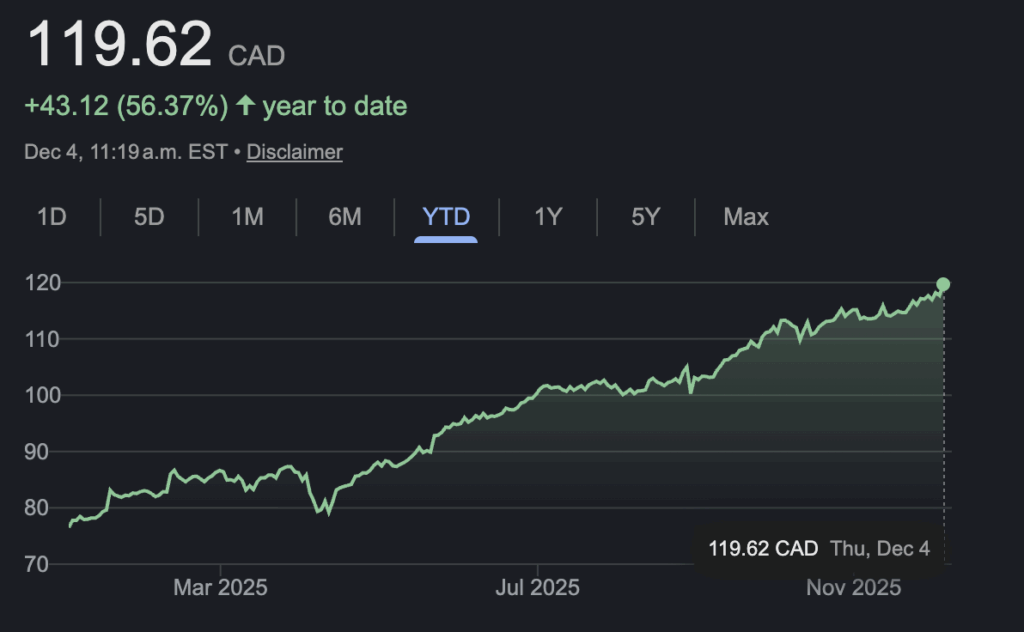

CIBC reports fourth-quarter profit up from year ago, raises dividend

CIBC (TSX:CM)

Numbers for its fourth quarter:

- Profit: $2.18 billion (up from $1.88 billion a year ago)

- Revenue: $7.58 billion (up from $6.62 billion)

CIBC raised its dividend as it reported a fourth-quarter profit of $2.18 billion, up from $1.88 billion a year ago. The bank said Thursday it will now pay a quarterly dividend of $1.07 per share, up from 97 cents per share. CIBC says its profit for the quarter ended Oct. 31 amounted to $2.20 per diluted share, up from $1.90 per diluted share a year ago.

Revenue for the quarter totalled $7.58 billion, up from $6.62 billion, while the bank’s provision for credit losses amounted to $605 million, up from $419 million a year ago. On an adjusted basis, CIBC says it earned $2.21 per diluted share, up from an adjusted profit of $1.91 per diluted share in the same quarter last year.

Analysts on average had expected an adjusted profit of $2.08 per share, according to estimates compiled by LSEG Data & Analytics.

“In a dynamic operating environment, our proactive and disciplined approach to managing our business, our resilient capital position and our deep client relationships supported robust growth while maintaining strong credit quality,” CIBC chief executive Harry Culham said in a statement.

CIBC said the growth came as its Canadian personal and business banking business earned $796 million in its latest quarter, up from $792 million a year ago as higher revenue was partially offset by a higher provision for credit losses and higher expenses.

The bank’s Canadian commercial banking and wealth management group earned $603 million, up from $551 million a year ago, while its U.S. commercial banking and wealth management business earned $275 million, up from $200 million a year ago.

CIBC’s capital markets business earned $548 million, up from $346 million in the same quarter last year.

CIBC also announced several senior executive changes Thursday that will be effective Jan. 1. The bank said Sandy Sharman, senior executive vice-president and group head, people, culture and brand, will transition to the role of special adviser before retiring at the end of 2026. CIBC also said Christina Kramer, senior executive vice-president and chief administrative officer, will add responsibility for enterprise real estate, enterprise capabilities and organizational agility, brand, community investment, client experience, communications, and corporate events. Richard Jardim will be appointed senior executive vice-president and chief technology and information officer, global technology, data and AI, while Yvonne Dimitroff will become executive vice-president and chief human resources officer, people, culture and talent.

Source Google

Source Google

BMO Financial Group reports $2.3B fourth-quarter profit, raises dividend

BMO Financial Group (TSX:BMO)

Numbers for its fourth quarter:

- Profit: $2.30 billion (compared to $2.30 billion a year ago)

- Revenue: $9.34 billion (up from $8.96 billion)

BMO Financial Group raised its dividend as it reported a fourth-quarter profit of $2.30 billion. The bank said Thursday it will now pay a quarterly dividend of $1.67 per share, an increase of four cents per share. BMO says its profit amounted to $2.97 per diluted share for the quarter ended Oct. 31 compared with a profit of $2.30 billion or $2.94 per diluted share a year ago when it had more shares outstanding.

Revenue for the quarter totalled $9.34 billion, up from $8.96 billion last year, while the bank’s provision for credit losses totalled $755 million, down from $1.52 billion a year ago. On an adjusted basis, BMO says it earned $3.28 per diluted share, up from an adjusted profit of $1.90 per diluted in the same quarter last year.

Analysts on average had expected an adjusted profit of $3.03 per share, according to estimates compiled by LSEG Data & Analytics.

“Fiscal 2025 was a strong year for BMO, with consistent execution and growing momentum to achieve our commitments to shareholders,” BMO chief executive Darryl White said. “We enter 2026 in a position of financial strength, with a focused strategy and a winning culture that continues to grow and attract talent across the bank.”

BMO said its Canadian personal and commercial banking business earned $752 million, up from $750 million a year ago, while its U.S. banking business earned $807 million, up from $281 million in the same quarter last year.

The bank’s wealth management arm earned $383 million, up from $301 million a year ago.

BMO’s capital markets business earned $521 million, up from $251 million in the same quarter last year.

The bank also announced Thursday the appointment of Tammy Brown to its board of directors.

Brown previously served as deputy chair of KPMG Canada’s board of directors and was a partner and national industry leader for industrial markets at the firm.

Source Google

Source Google

TD Bank reports $3.28B fourth-quarter profit, raises dividend

TD Bank Group (TSX:TD)

Numbers for its fourth quarter:

- Profit: $3.28 billion (down from $3.64 billion a year ago)

- Revenue: $15.49 billion (down from $15.51 billion)

TD Bank Group raised its dividend as it reported its fourth-quarter profit fell compared with a year ago, weighed down by one-time restructuring charges. The bank said Thursday it will pay a quarterly dividend of $1.08 per share, up from $1.05 per share.

TD says its profit amounted to $3.28 billion or $1.82 per diluted share for the quarter ended Oct. 31, compared with a profit of $3.64 billion or $1.97 per diluted share a year ago. On an adjusted basis, TD says it earned $2.18 per diluted share for its latest quarter, up from an adjusted profit of $1.72 per diluted share in the same quarter last year.

Revenue for the quarter totalled $15.49 billion, down from $15.51 billion a year ago, while the bank’s provision for credit losses amounted to $982 million, down from $1.11 billion in the same quarter last year.

Analysts on average had expected an adjusted profit of $2.03 per share, according to estimates compiled by LSEG Data & Analytics.

“TD had a strong fourth quarter, delivering robust fee and trading income in our markets-driven businesses as well as volume growth year-over-year in Canadian personal and commercial banking, capping a year of strong performance,” TD chief executive Raymond Chun said in a statement.

TD said its Canadian personal and commercial banking business earned $1.87 billion in its latest quarter, up from $1.82 billion a year ago as higher revenue was partially offset by higher provisions for credit losses and non-interest expenses.

The bank’s U.S. retail banking operations earned $719 million, up from $702 million in the same quarter last year.

TD’s wealth management business earned $699 million in the quarter, up from $349 million a year ago, while the bank’s wholesale baking group earned $494 million, up from $235 million in the same quarter last year.

Source Google

Source Google

Tools

MoneySense’s ETF Screener Tool

use tool

Read more news:

- News for investors: Barrick settles Mali dispute and Couche-Tard profit climbs

- Canadians aren’t as generous as they used to be

- Credit counselling calls surge as Canadians struggle with rising costs

- How cash ETFs keep your money working

The post Stock news for investors: Fourth-quarter earnings roll in from Canada’s big banks appeared first on MoneySense.

Market Opportunity

Rubic Price(RBC)

$0.005087

$0.005087$0.005087

USD

Rubic (RBC) Live Price Chart

Disclaimer: The articles reposted on this site are sourced from public platforms and are provided for informational purposes only. They do not necessarily reflect the views of MEXC. All rights remain with the original authors. If you believe any content infringes on third-party rights, please contact [email protected] for removal. MEXC makes no guarantees regarding the accuracy, completeness, or timeliness of the content and is not responsible for any actions taken based on the information provided. The content does not constitute financial, legal, or other professional advice, nor should it be considered a recommendation or endorsement by MEXC.

You May Also Like

Volante Technologies Customers Successfully Navigate Critical Regulatory Deadlines for EU SEPA Instant and Global SWIFT Cross-Border Payments

PaaS leader ensures seamless migrations and uninterrupted payment operations LONDON–(BUSINESS WIRE)–Volante Technologies, the global leader in Payments as a Service

Share

AI Journal2025/12/16 17:16

Fed Acts on Economic Signals with Rate Cut

In a significant pivot, the Federal Reserve reduced its benchmark interest rate following a prolonged ten-month hiatus. This decision, reflecting a strategic response to the current economic climate, has captured attention across financial sectors, with both market participants and policymakers keenly evaluating its potential impact.Continue Reading:Fed Acts on Economic Signals with Rate Cut

Share

Coinstats2025/09/18 02:28

Google's AP2 protocol has been released. Does encrypted AI still have a chance?

Following the MCP and A2A protocols, the AI Agent market has seen another blockbuster arrival: the Agent Payments Protocol (AP2), developed by Google. This will clearly further enhance AI Agents' autonomous multi-tasking capabilities, but the unfortunate reality is that it has little to do with web3AI. Let's take a closer look: What problem does AP2 solve? Simply put, the MCP protocol is like a universal hook, enabling AI agents to connect to various external tools and data sources; A2A is a team collaboration communication protocol that allows multiple AI agents to cooperate with each other to complete complex tasks; AP2 completes the last piece of the puzzle - payment capability. In other words, MCP opens up connectivity, A2A promotes collaboration efficiency, and AP2 achieves value exchange. The arrival of AP2 truly injects "soul" into the autonomous collaboration and task execution of Multi-Agents. Imagine AI Agents connecting Qunar, Meituan, and Didi to complete the booking of flights, hotels, and car rentals, but then getting stuck at the point of "self-payment." What's the point of all that multitasking? So, remember this: AP2 is an extension of MCP+A2A, solving the last mile problem of AI Agent automated execution. What are the technical highlights of AP2? The core innovation of AP2 is the Mandates mechanism, which is divided into real-time authorization mode and delegated authorization mode. Real-time authorization is easy to understand. The AI Agent finds the product and shows it to you. The operation can only be performed after the user signs. Delegated authorization requires the user to set rules in advance, such as only buying the iPhone 17 when the price drops to 5,000. The AI Agent monitors the trigger conditions and executes automatically. The implementation logic is cryptographically signed using Verifiable Credentials (VCs). Users can set complex commission conditions, including price ranges, time limits, and payment method priorities, forming a tamper-proof digital contract. Once signed, the AI Agent executes according to the conditions, with VCs ensuring auditability and security at every step. Of particular note is the "A2A x402" extension, a technical component developed by Google specifically for crypto payments, developed in collaboration with Coinbase and the Ethereum Foundation. This extension enables AI Agents to seamlessly process stablecoins, ETH, and other blockchain assets, supporting native payment scenarios within the Web3 ecosystem. What kind of imagination space can AP2 bring? After analyzing the technical principles, do you think that's it? Yes, in fact, the AP2 is boring when it is disassembled alone. Its real charm lies in connecting and opening up the "MCP+A2A+AP2" technology stack, completely opening up the complete link of AI Agent's autonomous analysis+execution+payment. From now on, AI Agents can open up many application scenarios. For example, AI Agents for stock investment and financial management can help us monitor the market 24/7 and conduct independent transactions. Enterprise procurement AI Agents can automatically replenish and renew without human intervention. AP2's complementary payment capabilities will further expand the penetration of the Agent-to-Agent economy into more scenarios. Google obviously understands that after the technical framework is established, the ecological implementation must be relied upon, so it has brought in more than 60 partners to develop it, almost covering the entire payment and business ecosystem. Interestingly, it also involves major Crypto players such as Ethereum, Coinbase, MetaMask, and Sui. Combined with the current trend of currency and stock integration, the imagination space has been doubled. Is web3 AI really dead? Not entirely. Google's AP2 looks complete, but it only achieves technical compatibility with Crypto payments. It can only be regarded as an extension of the traditional authorization framework and belongs to the category of automated execution. There is a "paradigm" difference between it and the autonomous asset management pursued by pure Crypto native solutions. The Crypto-native solutions under exploration are taking the "decentralized custody + on-chain verification" route, including AI Agent autonomous asset management, AI Agent autonomous transactions (DeFAI), AI Agent digital identity and on-chain reputation system (ERC-8004...), AI Agent on-chain governance DAO framework, AI Agent NPC and digital avatars, and many other interesting and fun directions. Ultimately, once users get used to AI Agent payments in traditional fields, their acceptance of AI Agents autonomously owning digital assets will also increase. And for those scenarios that AP2 cannot reach, such as anonymous transactions, censorship-resistant payments, and decentralized asset management, there will always be a time for crypto-native solutions to show their strength? The two are more likely to be complementary rather than competitive, but to be honest, the key technological advancements behind AI Agents currently all come from web2AI, and web3AI still needs to keep up the good work!

Share

PANews2025/09/18 07:00